This article originally appeared at Your Local Epidemiologist New York. Sign up for the YLE NY newsletter here. Public health, explained: Sign up to receive Healthbeat’s free New York City newsletter here.

If ACA subsidies expire, someone making just $1 over the cutoff could pay $5,000–$10,000 more per year for health insurance.

For those who are older, it could be even higher. Let’s break down what that means (and give an update on respiratory viruses at the end).

The longest government shutdown in U.S. history is over. Wednesday night, the president signed a bill that narrowly passed the House. The government is officially reopened.

But even as Washington moves to turn the lights back on after more than 40 days, another major fight over health policy looms. Republicans have promised to bring a separate vote in December on whether to extend the expanded Affordable Care Act subsidies, which are set to expire at the end of the year. These subsidies, introduced during the pandemic through the 2021 American Rescue Plan and extended by the 2022 Inflation Reduction Act, made health insurance more affordable for millions of Americans.

If they expire at the end of the year, health care will become more expensive for millions. But first, some background.

What’s ‘the marketplace’?

The marketplace (also called the exchange) is the online platform set up under the ACA where individuals can shop for, compare, and enroll in health insurance plans that meet specific government standards. It’s especially important for those who don’t get insurance through their jobs.

- In New York, the marketplace is called the New York State of Health.

- The ACA marketplace open enrollment period for 2026 coverage started Nov. 1 and runs through Jan. 15. Some states have different deadlines.

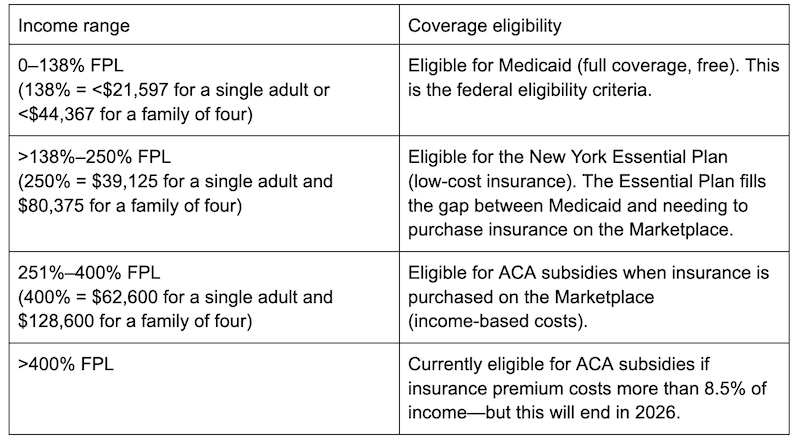

New York’s coverage framework: Who’s covered

Under the ACA, there are four tiers of coverage in New York based on income, using the percent of the Federal Poverty Level. These income thresholds are adjusted each year to reflect inflation. Here’s how it breaks down for 2025:

Return of the ‘subsidy cliff’ and what the 400% FPL line really means

Before 2021, people who earned even just $1 over the 400% FPL got zero help, regardless of how expensive their insurance costs were. This was called the “subsidy cliff.” During the pandemic, the subsidy cliff was removed, letting anyone get help if premiums were unaffordable (greater than 8.5% of one’s income).

Now, with the new federal budget, the subsidy cliff is set to return next year. Those making just above 400% of the FPL — roughly $60,000 for an individual or $124,000 for a family of four — will be hit hardest if the expanded ACA subsidies expire. These middle-income families could see the steepest increases in their insurance costs.

A real-world example: a single adult in NYC

Take a hypothetical single adult living in New York City, making $63,000 per year — just over 400% of the FPL. Their employer doesn’t offer insurance. Today, with ACA subsidies, they would pay $446/month for a basic, silver plan from the marketplace ($5,335 annually). This is 8.5% of their income, capped by the federal limit.

Next year, without the subsidies, they would pay the full cost, around $867 per month ($10,404 annually). It almost doubles the price. This, compounded by the high cost of living in New York (with the average monthly rent for a studio apartment in New York City running about $2,500), could have serious consequences.

You can estimate your own insurance costs here through KFF.

For older adults, the costs hit even harder

Insurance premiums rise with age. Older adults tend to use more health care, more often, for more complex or chronic health issues, and insurers use age to price risk. A couple in New York City making $85,000 per year (402% of the FPL limit) would currently expect to pay about $602 per month ($7,224 annually) for a silver plan. Without the ACA subsidies, that would go up to about $1,734 ($20,808 annually)—almost triple the cost, and about a quarter of their total income. When accounting for rising premium costs, especially for older adults, it would likely be higher.

This couple could see annual insurance costs jump by more than $13,000 — a cost that would have significant implications for someone’s budget and any emergency cushion.

The takeaways

- New Yorkers with the lowest incomes, who qualify for Medicaid or the New York Essential Plan (<250% FPL), will be insulated from these changes — this safety net is holding.

- Many New Yorkers, especially older adults who don’t yet qualify for Medicaid (<65) and middle-income individuals without employer-sponsored health insurance, will face steep increases in insurance costs.

- The “subsidy cliff” will return, causing those with incomes just above the threshold to face the highest cost increases.

If you’re unsure what you or your loved ones qualify for, visit nystateofhealth.ny.gov.

This debate isn’t over yet, so now’s a good time to understand what’s at stake. We’ll be watching closely.

Infectious disease ‘weather report’

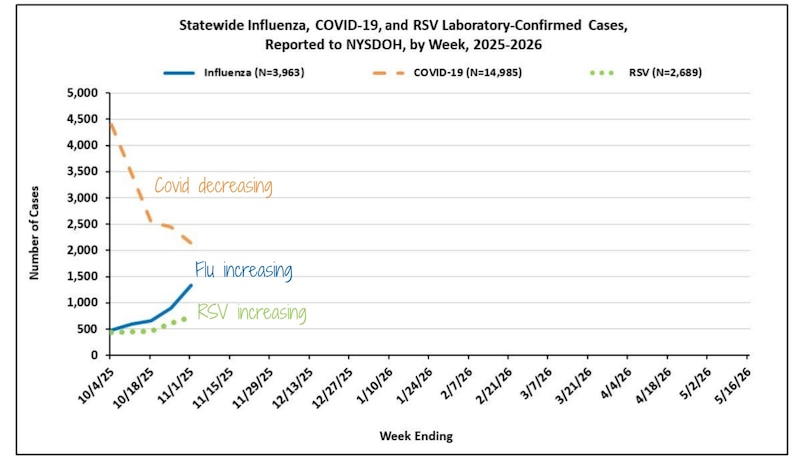

Covid-19: Cases and hospitalizations are decreasing in both New York City and across the state. However, wastewater data (via Biobot and WastewaterSCAN) are showing signs of an increase in the Northeast and South. This could mean that we start seeing more cases and hospitalizations for Covid in the next few weeks.

Flu: Flu is increasing quickly. The most recent data show that cases and hospitalizations in New York have increased by 49% and 71%, respectively. In New York City, emergency department visits for the flu rose by 83%.

RSV: Also increasing across the state and in New York City, mostly in kids under 4. Statewide, cases increased by 19%, while emergency department visits in New York City went up by 67%.

Data from the New York Department of Health shows that Covid vaccinations in the state are down by 30% compared to this time last year. Doses for those over 65, the group most vulnerable to severe illness, are down ~25%. With fewer New Yorkers getting vaccinated, our collective defenses are weaker.

As we head into the holidays, where many of us will pass through crowded airports and spend time with young and old family members, vaccination remains our best bet to protect ourselves and our loved ones.

It’s still a great time to get vaccinated. In New York, anyone over 3 years old can be vaccinated at a pharmacy. Kids under 3 need to get their Covid vaccines from a pediatric provider, like their pediatrician. Make sure to call ahead to ensure that the provider has pediatric doses of the Covid vaccine.

Bottom line

If Congress lets the expanded ACA subsidies expire, many middle-income New Yorkers, especially those just above the 400% federal poverty limit, could see their health insurance costs substantially increase. For older adults, this could hit even harder. Now’s a good time to stay informed about what’s being discussed in Washington.

Love,

Your NY Epi

Dr. Marisa Donnelly, PhD, is an epidemiologist, science communicator, and public health advocate. She specializes in infectious diseases, outbreak response, and emerging health threats. She has led multiple outbreak investigations at the California Department of Public Health and served as an Epidemic Intelligence Service Officer at the Centers for Disease Control and Prevention. Donnelly is also an epidemiologist at Biobot Analytics, where she works at the forefront of wastewater-based disease surveillance.